API Security for Fintech in GCC: A Smart Guide

API Security for Fintech in GCC: A Smart Guide

API Security for Fintech in GCC: A Smart Guide

API security for fintech in GCC is now a trust issue, not just a technical checklist. Banks, wallets, payment platforms, lending apps, remittance providers, and eKYC systems across Saudi Arabia, the UAE, and Qatar all depend on APIs to move sensitive financial data safely.

In simple terms, API security for fintech in GCC means protecting payment, identity, consent, and banking APIs with strong authentication, bot defense, rate limiting, encryption, monitoring, and compliant data handling. For fintech teams in Riyadh, Dubai, Abu Dhabi, and Doha, the goal is clear: keep customer data private, reduce fraud, and support secure digital finance growth.

Why GCC Fintech APIs Are High-Risk Targets

Fintech growth across the GCC is moving fast. Customers now expect instant onboarding, mobile wallets, open banking features, digital payments, and smooth identity verification.

Behind that smooth experience, APIs are doing most of the heavy lifting.

They connect mobile apps to banks, checkout pages to payment gateways, eKYC tools to onboarding flows, and fraud engines to transaction systems. That makes every exposed endpoint a potential target.

A weak fintech API can leak account details, expose KYC records, trigger fraudulent payments, or let bots abuse onboarding and rewards systems. For regulated financial products, that risk can quickly become a compliance, reputation, and customer trust problem.

Saudi Arabia’s open banking framework includes use cases, business rules, and technical standards for customer-permissioned data sharing. UAE PASS is the UAE’s secure national digital identity for citizens, residents, and visitors. Qatar Central Bank also highlights fintech strategy, payment services regulation, and eKYC resources as part of its financial technology ecosystem.

What Is API Security for Fintech in GCC?

API security for fintech in GCC means protecting the interfaces that handle financial data, identity records, payment instructions, consent permissions, wallet balances, and transaction activity.

A normal business API may expose product listings or booking details. A fintech API can expose bank account information, transaction history, customer identity documents, authentication tokens, and payment commands.

That is why fintech APIs need tighter controls than general business APIs.

Common GCC fintech API use cases include.

Payment gateway integrations

Open banking connections

Digital wallets

Buy-now-pay-later platforms

Remittance apps

eKYC onboarding

Mobile banking features

Fraud monitoring tools

Customer consent dashboards

For example, a Dubai e-commerce business adding a wallet feature may need secure API integrations between its mobile app, checkout system, fraud engine, and payment provider. Mak It Solutions’ mobile app development services can help plan secure app architecture from the first release.

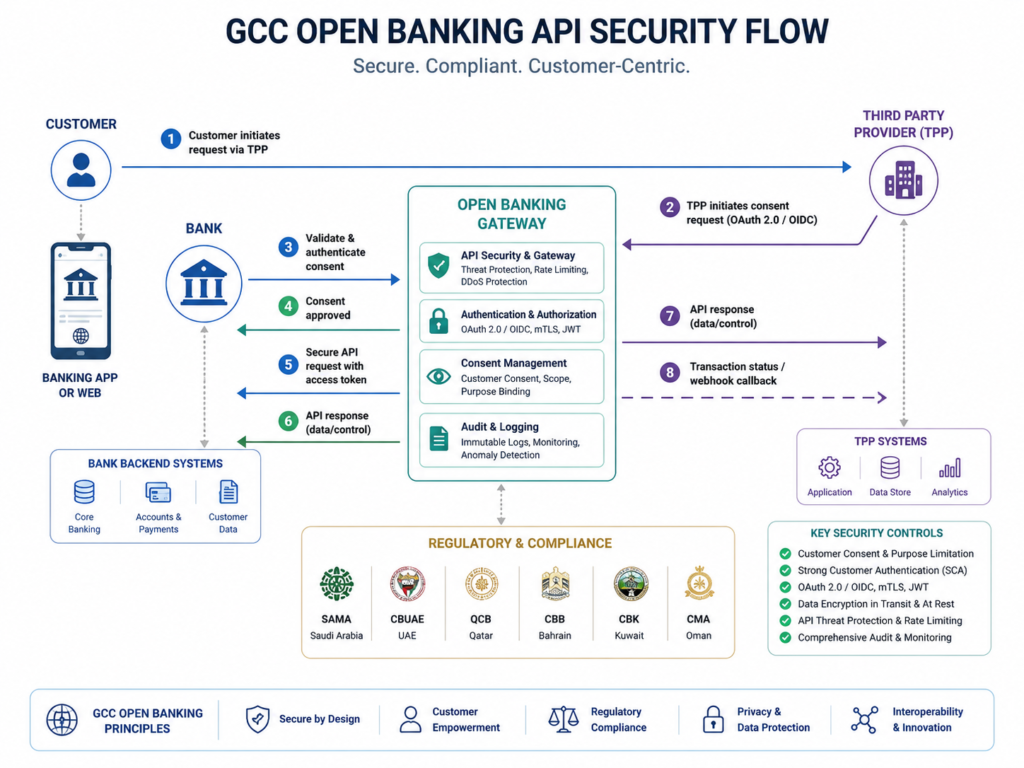

Why Open Banking Makes API Security Critical

Open banking creates better financial experiences, but it also increases exposure.

More partners means more tokens, more consent flows, more third-party integrations, and more customer data moving between systems. If those APIs are not properly secured, attackers can exploit gaps in authentication, authorization, rate limits, or monitoring.

Saudi Open Banking and API Risk

Saudi fintech teams working around open banking should design security early.

That means using strong authentication, mutual TLS where required, scoped access, encryption, audit logs, rate limiting, consent records, and incident response planning. SAMA’s open banking direction supports financial innovation and customer-permissioned data sharing, so secure API design is central to the model.

For a Riyadh fintech startup, security should not be added after launch. It should shape the API architecture from day one.

UAE Open Finance, UAE PASS, DIFC, and ADGM

In the UAE, fintech platforms may operate across Dubai, Abu Dhabi, DIFC, ADGM, or wider mainland environments.

APIs connected to identity, payments, onboarding, and user sessions need extra care. UAE PASS is widely positioned as a secure national digital identity, so fintech apps integrating with it must protect callback URLs, tokens, mobile deep links, session handling, and consent journeys.

A smooth login is important. A secure login is essential.

Qatar’s Growing Fintech Ecosystem

Qatar’s fintech ecosystem is also developing around digital finance, payments, eKYC, and market infrastructure. Qatar Central Bank lists financial technology resources that include fintech strategy, payment services regulation, and eKYC regulations.

For a Doha fintech platform, API security should cover partner integrations, monitoring, cloud architecture, customer consent, and data governance from the beginning.

Key API Threats Facing GCC Fintech Platforms

Bot Attacks, Scraping, and Fake Accounts

Bots often target onboarding forms, referral programs, wallet rewards, price feeds, login pages, and public APIs.

For GCC fintech platforms, bots may also abuse bilingual forms, OTP flows, SMS verification, and promotional campaigns. If the backend trusts the mobile app too much, attackers can bypass the front-end and hit APIs directly.

Strong bot protection should include device signals, behavioral analysis, rate limits, API schema checks, and fraud scoring.

Credential Stuffing and Account Takeover

Credential stuffing happens when attackers reuse leaked usernames and passwords from other platforms.

For fintech apps, this can lead to account takeover, unauthorized transactions, wallet abuse, or sensitive data exposure.

Good protection combines multi-factor authentication, device fingerprinting, suspicious login detection, user alerts in Arabic and English, and account recovery controls that do not create new loopholes.

API Cost Abuse and Rate-Limit Bypass

Attackers may abuse expensive APIs, trigger repeated verification calls, scrape data, or overload backend services.

Rate limiting helps, but it should not be the only control. Fintech teams also need throttling, abuse detection, partner-level quotas, logging, and alerts for unusual traffic patterns.

For stronger customer portals and backend systems, GCC teams can combine secure architecture with Mak It Solutions’ PHP web development services or front-end development services.

Core API Security Controls for GCC Fintechs

API Gateway, WAF, and Bot Mitigation

An API gateway helps centralize access control, traffic routing, authentication, logging, and throttling.

A WAF adds another layer by blocking common web attacks. Bot mitigation helps identify automated abuse before it reaches payment, wallet, or identity systems.

Together, these controls reduce noise, block suspicious traffic, and give security teams clearer visibility.

Strong Authentication and Consent Management

Fintech APIs should use strong authentication, short-lived tokens, scoped permissions, secure token storage, and consent controls.

For open banking and digital finance, consent must be easy to understand. In GCC markets, that often means Arabic and English consent screens, plain wording, masked data previews, and simple revocation options.

Security fails when users do not understand what they approved.

Rate Limiting, Throttling, and Monitoring

Rate limiting reduces brute-force attacks, scraping, and API cost abuse.

Throttling helps slow suspicious behavior without fully blocking legitimate customers. Monitoring helps detect unusual login velocity, repeated OTP requests, transaction spikes, partner abuse, or abnormal API calls.

In practice, fintech teams should monitor both technical events and business signals.

GCC Compliance, Data Residency, and Trust Requirements

Saudi Arabia.

Saudi fintechs should treat API logs, consent records, customer identifiers, token activity, and data retention as governance assets.

That does not mean every product has the same regulatory burden. A payment app, lending platform, wallet, and analytics tool may each face different expectations.

Still, the direction is clear: customer data, permissions, and financial activity must be handled with care.

UAE.

UAE fintech teams should pay close attention to APIs connected to identity, payments, onboarding, and customer records.

Digital identity is becoming central to both public and private services, and UAE PASS sits at the heart of many identity journeys. That makes secure integration patterns, session protection, and login abuse testing especially important.

Qatar.

Qatar fintech teams should consider QCB guidance, eKYC requirements, payment services rules, and local data governance expectations when designing APIs.

A Doha-based fintech handling sensitive data should think carefully about where API logs, backups, analytics, and customer records are stored and processed.

For content-led growth in Qatar and the wider GCC, Mak It Solutions’ SEO services can help explain technical and compliance-heavy products in a clearer way.

How to Build a Secure Fintech API Strategy in the GCC

A secure API strategy does not start with tools. It starts with visibility.

Start with API Inventory and Risk Classification

List every API your platform uses.

Include the owner, data type, authentication method, partner access, business impact, and exposure level. Then classify APIs as public, partner, internal, sensitive, or regulated.

This helps teams decide which APIs need stricter authentication, deeper monitoring, or more frequent testing.

Design for Arabic UX and Secure Consent

Many GCC fintech platforms serve Arabic and English users.

Consent screens, permission prompts, error messages, and security alerts should be clear in both languages. Avoid legal-heavy wording where plain language works better.

A good consent flow should explain.

What data is being shared

Who it is shared with

Why it is needed

How long access lasts

How the user can revoke access

Choose Cloud and Hosting Models Carefully

Cloud location matters for latency, resilience, compliance, and data governance.

Regional infrastructure options from major cloud providers can support GCC workloads, but fintech teams should still review where data, logs, backups, and analytics are stored. Google Cloud lists global cloud regions for low latency and availability, while Microsoft notes that Azure geographies are designed to support data residency and compliance needs.

For sensitive fintech systems, the cloud decision should involve security, legal, compliance, and engineering teams together.

Choosing an API Security Partner for GCC Fintech Growth

A good API security partner should understand more than code.

For Saudi, UAE, and Qatar fintech projects, look for secure architecture experience, API integration skills, fintech awareness, bilingual UX understanding, and cloud-readiness.

Mak It Solutions’ services overview is a useful starting point for web, mobile, SaaS, and integration planning.

Before choosing a partner, ask practical questions.

Can they design secure API logging and alerting?

Do they understand token lifecycle controls?

Can they test APIs before production?

Do they plan for mobile API abuse?

Can they support secure partner onboarding?

Do they understand Arabic and English user flows?

Can they help with fraud monitoring and access control?

A small wallet app may begin with gateway controls, WAF rules, and rate limits. A regulated open banking provider may need a full API security platform, continuous testing, partner governance, and deeper threat detection.

Final Thoughts

API security for fintech in GCC protects growth, not just systems.

Customers in Riyadh, Jeddah, Dubai, Abu Dhabi, and Doha will only trust digital finance when the experience feels fast, local, private, and safe. For fintech platforms, that means combining API gateway security, strong authentication, consent management, bot protection, data governance, and fraud monitoring from day one.

Planning a fintech app, wallet, SaaS platform, or secure API integration for the GCC? Contact Mak It Solutions to build a practical security-first roadmap for Saudi, UAE, and Qatar markets. You can also explore web designing services, React Native development, or digital marketing support for your next GCC launch.

FAQs

Q : Is API security required for Saudi fintech companies?

A : Yes. Any Saudi fintech working with banking, payments, wallets, lending, or open banking data should treat API security as a core requirement. Strong authentication, encryption, rate limiting, monitoring, audit logs, and incident response planning should be built before scale.

Q : How should UAE fintech apps secure APIs connected to UAE PASS?

A : UAE fintech apps should secure authentication flows, callback URLs, token handling, mobile deep links, session management, and consent journeys. Teams should also test for replay attacks, account takeover, login abuse, and weak mobile-to-API trust.

Q : What API security controls matter most for Qatar fintech companies?

A : Qatar fintech companies should focus on API discovery, access control, encryption, eKYC protection, rate limiting, partner risk reviews, cloud governance, and real-time monitoring. Data handling, log storage, and customer consent should also be reviewed early.

Q : Do GCC fintech mobile apps need bot protection?

A : Yes. Mobile fintech apps are common targets for fake registrations, referral abuse, credential stuffing, scraping, OTP abuse, and wallet fraud. Bot protection should work at the API level because attackers can often bypass the visible mobile interface.

Q : How does data residency affect API security for fintech in GCC?

A : Data residency affects where customer data, API logs, backups, analytics, and identity records are stored or processed. GCC fintech teams should align architecture decisions with local governance expectations, product risk, and regulatory obligations.