Arabic LLMs for Banking: Saudi & UAE Guide

Arabic LLMs for Banking: Saudi & UAE Guide

Arabic LLMs for Banking: Saudi & UAE Guide

Arabic LLMs for banking help GCC financial institutions serve Arabic-speaking customers, review KYC documents, detect fraud signals, and support compliance teams with localized AI. For banks in Saudi Arabia, the UAE, and Qatar, the biggest value comes when Arabic AI is deployed with clear data governance, audit logs, explainability, and human oversight.

Arabic LLMs should not replace regulated decisions in KYC, AML, credit, or fraud enforcement. Used well, they work as a decision-support layer that helps teams move faster without losing control.

Why Arabic LLMs Matter for GCC Banking

GCC banks are moving quickly toward digital-first banking. In Riyadh, Dubai, Abu Dhabi, Doha, and Jeddah, customers expect instant Arabic support, smooth onboarding, secure payments, and trusted mobile experiences.

But many English-first AI systems still struggle with Arabic names, Gulf dialects, transliteration, mixed Arabic-English messages, and local regulatory language.

That is where Arabic LLMs for banking become important. They can help banks improve Arabic customer service, KYC automation, AML review, fraud-alert triage, compliance search, and risk analysis as long as they are implemented responsibly.

For GCC banks, the goal is not “AI everywhere.” The real goal is safer, faster, more localized banking operations.

What Are Arabic LLMs for Banking?

Arabic LLMs for banking are large language models trained, fine-tuned, or adapted to understand Arabic financial language, customer conversations, documents, policies, and compliance workflows.

Instead of simply translating English outputs into Arabic, Arabic-native or Arabic-optimized models can understand context more naturally. This matters in banking because small language errors can create real compliance, customer experience, and fraud-risk problems.

How Arabic LLMs differ from generic English LLMs

Generic models may misunderstand.

Arabic spelling variations

Gulf dialects

Arabic-English mixed messages

Name transliteration

Banking terminology

Regulatory wording

Customer intent in support chats

For example, the same customer name may appear as “Mohammed,” “Muhammad,” “Mohamad,” or in Arabic script. A banking AI system must handle those variations carefully without creating too many false positives.

Why Saudi, UAE, and Qatar banks need Arabic-native AI

Saudi banks are operating in a fast digital transformation environment. UAE banks often serve multilingual customers across mainland and financial-free-zone contexts. Qatar banks are expanding fintech and digital-service capabilities while aligning with national financial-sector priorities.

In all three markets, Arabic AI needs to respect language, regulation, privacy, and trust.

Where Arabic LLMs fit in banking workflows

Arabic LLMs can support.

Customer onboarding

Arabic contact centers

KYC document review

AML alert summaries

Fraud operations

Risk memo preparation

Internal knowledge search

Policy and compliance assistance

For banks building secure digital portals or internal dashboards, Mak It Solutions’ custom software and web development services can support the front-end and back-end foundations.

Key Use Cases for Arabic LLMs in GCC Banking

Arabic LLMs for banking are most useful when they reduce manual effort without replacing regulated judgment.

They should help teams read, summarize, compare, classify, and route information. Final decisions should remain with authorized people, especially in KYC, AML, fraud, credit, and customer-risk workflows.

Arabic customer support and banking chatbots

A UAE bank can use an Arabic chatbot to answer common questions about accounts, cards, wallets, transfers, branch services, and digital banking.

The chatbot can respond in Modern Standard Arabic or a controlled Gulf Arabic tone, depending on the bank’s brand and customer base. It can also detect when a customer is confused, upset, or reporting a possible scam.

For mobile-first banking journeys, mobile app development services can help create secure Arabic customer experiences.

Internal copilots for relationship managers and operations teams

A relationship manager in Riyadh could ask an internal copilot to summarize a corporate customer profile, previous interactions, pending documents, and recent account activity.

The key word is “internal.” The copilot should only use approved bank data, follow role-based access controls, and record activity for audit.

In practice, this can save time for relationship managers, branch teams, onboarding staff, and operations units without exposing sensitive data to uncontrolled tools.

Document summarization for compliance, onboarding, and risk teams

Arabic NLP can summarize.

Trade licenses

Bank statements

Customer notes

Corporate documents

Policy documents

Regulatory circulars

Source-of-funds explanations

For regulated teams, this reduces review time while keeping human approval in place.

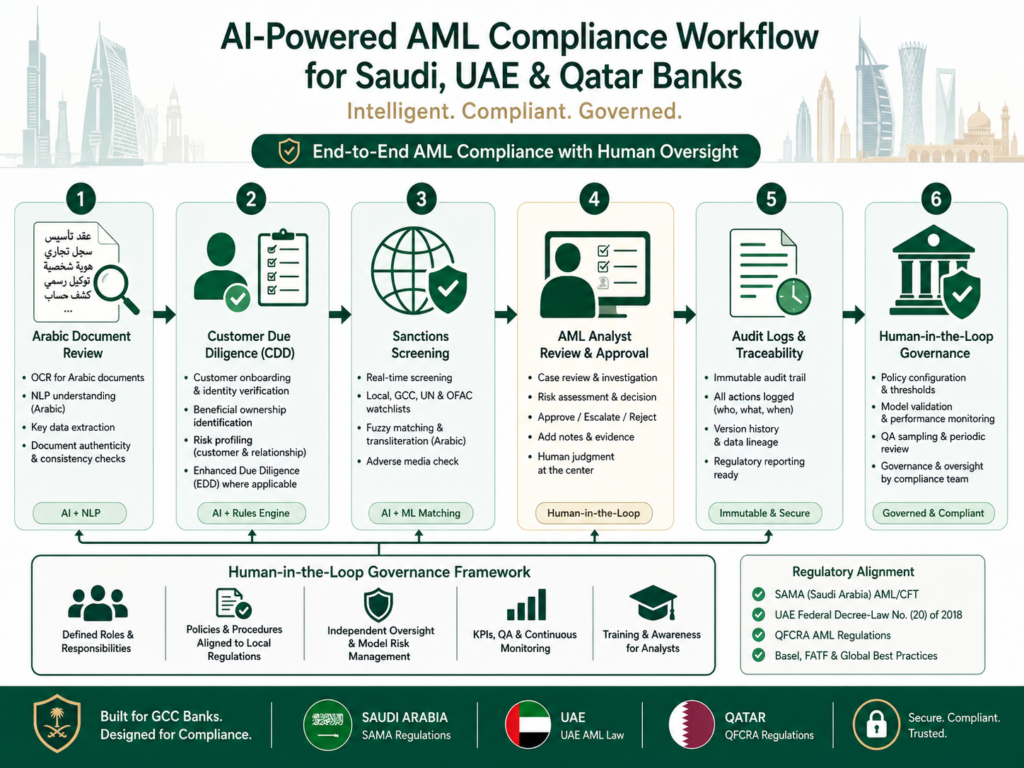

Arabic LLMs for KYC, AML, and Customer Due Diligence

KYC is one of the strongest use cases for Arabic LLMs for banking because GCC institutions often handle Arabic names, English transliterations, cross-border documentation, and complex ownership structures.

Improving Arabic name matching and fuzzy screening

Arabic LLMs can help compare customer names across IDs, sanctions lists, onboarding forms, and transaction records.

They can flag possible matches while reducing false positives caused by spelling differences. This is especially useful when Arabic names are converted into English in several different ways.

Still, name matching must be treated carefully. A model should suggest potential matches, explain why they were flagged, and pass them to a trained analyst for review.

Supporting eKYC automation in Saudi, UAE, and Qatar

A Saudi fintech in Riyadh may use AI to pre-check uploaded documents before human review. A UAE digital bank may combine AI-assisted onboarding with approved identity workflows. A Doha SME banking platform may use localized Arabic forms to reduce onboarding friction.

Good eKYC automation can help teams.

Extract key fields from documents

Detect missing information

Compare customer details

Summarize risk indicators

Route high-risk cases to analysts

SAMA emphasizes that financial institutions must protect customer personal data and apply proper controls for its security, integrity, and use.

Human-in-the-loop review for AML and high-risk customers

AI-powered AML compliance should not approve or reject high-risk customers on its own.

A safer model is simple: AI prepares the case summary, highlights risk indicators, shows supporting evidence, and routes complex cases to compliance analysts. The final decision remains with the bank’s approved process.

This matters because AML, sanctions, politically exposed person screening, and customer due diligence require judgment, documentation, and accountability.

AI Fraud Detection and Transaction Monitoring in GCC Banks

Fraud teams need speed, context, and explainability. Arabic LLMs can help review alerts faster, especially when fraud signals appear in Arabic messages, chat logs, complaints, or support conversations.

Detecting account takeover, payment fraud, and mule activity

Banks can combine transaction monitoring with language analysis to detect suspicious patterns such as.

Sudden beneficiary changes

Unusual transfer behavior

Scam-related customer messages

Repeated OTP-related complaints

Mule-account indicators

Suspicious wallet or card activity

Arabic LLMs can help summarize why an alert looks risky. That gives fraud analysts a clearer starting point.

Using Arabic NLP to analyze customer messages and fraud alerts

Arabic NLP can classify complaints, scam reports, and suspicious chat messages.

For example, a customer message mentioning an “OTP,” an urgent transfer, and an unknown caller can be escalated quickly. This helps fraud teams respond faster when minutes matter.

Applying AI across cards, wallets, open banking, and digital payments

Digital banking creates more touchpoints: cards, wallets, instant payments, open banking, merchant payments, and app-based transfers.

AI can help detect abnormal behavior across these channels, but it must integrate securely with core banking and monitoring systems. For secure customer portals, Mak It Solutions’ PHP web development services and front-end development services can support scalable banking interfaces.

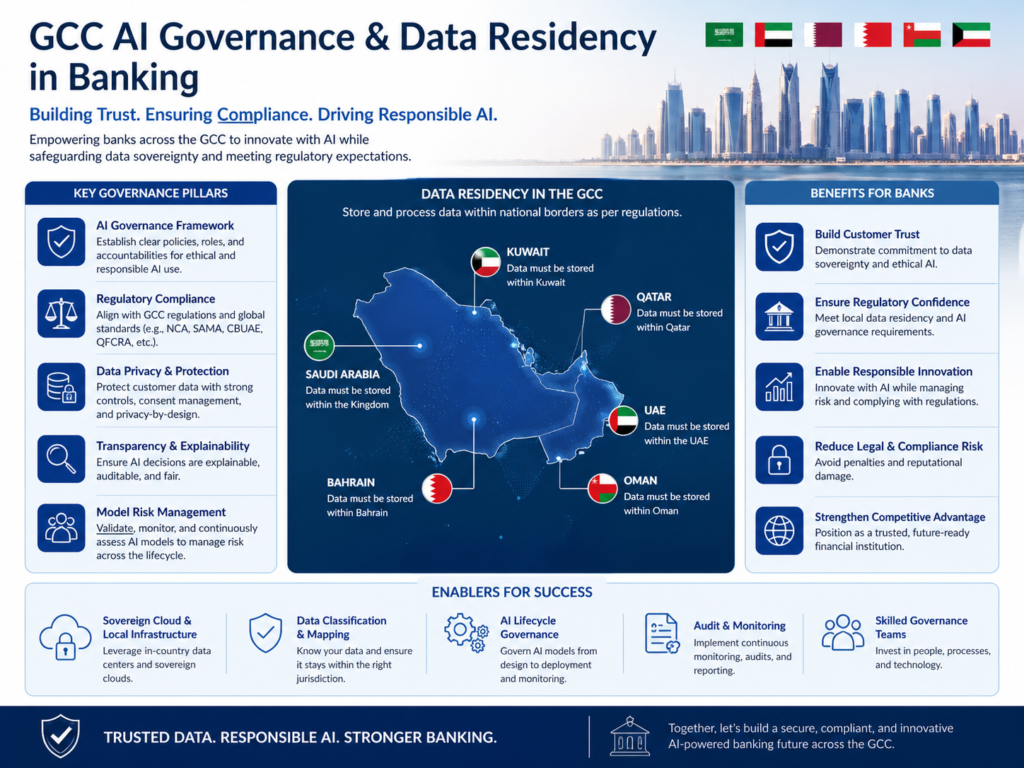

Compliance, Data Residency, and AI Governance in the GCC

Trust matters more than hype in banking AI.

Regulators expect financial institutions to control data, document risks, protect customers, and explain technology decisions. Arabic LLMs must therefore be treated as governed systems, not experimental chat tools.

Saudi banking AI considerations: SAMA, NDMO, and data controls

Saudi banks should align Arabic LLM projects with SAMA expectations, customer-data protection, cybersecurity, IT governance, and NDMO-related data principles.

SAMA’s IT Governance Framework defines principles and objectives for implementing and improving IT governance controls within regulated member organizations. It also emphasizes strict compliance with customer personal-data protection requirements.

For Arabic LLM projects, that means banks should define.

What data the model can access

Who can use the system

Where prompts and outputs are stored

How audit logs are reviewed

Which use cases require human approval

How customer data is protected

UAE banking AI considerations: CBUAE, TDRA, DIFC, and ADGM

In the UAE, banks should consider Central Bank of the UAE requirements, TDRA digital guidance, and data expectations in DIFC or ADGM where relevant.

The CBUAE rulebook expects institutions using material big data analytics and AI applications to ensure models are reliable, transparent, and explainable. Its AI-related consumer-protection guidance also focuses on responsible adoption and use of AI and machine-learning technologies by licensed financial institutions.

For UAE banks, this makes explainability and customer transparency especially important.

Qatar banking AI considerations: QCB and financial-sector data handling

Qatar banks should align AI projects with QCB expectations for financial-sector governance, data handling, and fintech innovation.

Qatar Central Bank issued an Artificial Intelligence Guideline on September 04, 2024, to regulate AI use within the financial sector. QCB’s fintech page also lists Artificial Intelligence Guidelines as part of its financial-technology resources.

For Doha-based banks and fintechs, this means AI use cases should be transparent, risk-based, tested, and documented before scaling.

How Banks Should Evaluate Arabic LLM Solutions

Choosing the right Arabic LLM is not only a technology decision. It is also a governance, risk, compliance, Arabic-accuracy, and integration decision.

Private LLM vs public LLM vs vendor-managed AI platform

| Option | Best for | Main concern |

|---|---|---|

| Private Arabic LLM | High-control banking environments | Cost, infrastructure, AI talent |

| Public LLM | Low-risk experiments and general productivity | Data privacy and regulatory limits |

| Vendor-managed AI platform | Faster pilots with support | Contract terms, hosting, audit logs |

Private LLMs give more control but require stronger infrastructure. Public LLMs are easier to start with but may create data concerns. Vendor-managed platforms can work well when hosting, access control, data usage, and audit rights are clearly defined.

Model explain ability, audit logs, and risk controls

Banks should require.

Explainable outputs

Prompt and response logging

Role-based access control

Red-team testing

Data-loss prevention controls

Human approval workflows

Model performance monitoring

Clear escalation rules

No compliance officer wants a black-box recommendation with no evidence trail.

Arabic accuracy, dialect coverage, and integration readiness

Banks should test Saudi, Emirati, Qatari, and broader Gulf Arabic. They should also test transliterated names, mixed Arabic-English text, and banking-specific terminology.

A model that performs well in a demo may still fail on real customer language.

For app-based banking products, React Native development services can support cross-platform digital experiences.

Best Practices for Implementing Arabic LLMs in GCC Banking

Start with low-risk pilots before regulated decisioning

Begin with low-risk internal use cases such as.

Internal FAQ search

Policy summarization

Training support

Document summaries

Customer-support drafting

Fraud-alert triage notes

Avoid direct AML, credit, fraud-enforcement, or customer-risk decisions until governance is mature.

Keep humans in the loop for KYC, AML, fraud, and credit decisions

A Riyadh fintech can use AI to prepare KYC summaries, but a compliance analyst should approve final actions.

A Dubai wallet provider can use AI to flag fraud patterns, while fraud teams confirm enforcement.

A Doha bank can use Arabic AI for customer-support and compliance-search workflows while keeping sensitive decisions supervised.

This approach gives teams speed without losing accountability.

Design for Arabic UX, privacy, and regional cloud requirements

Arabic AI should not feel like an English product with Arabic text pasted on top.

Banks should design for

Right-to-left interfaces

Arabic error messages

Dialect-aware support flows

Clear consent language

Secure authentication

Data-residency planning

Mobile-first customer journeys

Regional cloud strategy also matters. Google Cloud announced its Doha region in 2023 and described it as supporting Qatar’s data residency and digital-sovereignty needs.

For customer-facing platforms, Mak It Solutions can also support e-commerce integrations and SEO visibility for fintech education hubs.

Common Implementation Mistakes to Avoid

Arabic LLMs can create real value, but only when banks avoid common mistakes.

Treating Arabic AI as only a translation layer

Translation is not enough. Banking AI must understand Arabic context, intent, names, documents, and risk language.

Connecting sensitive data too early

Do not connect a model to production customer data before access controls, logging, privacy review, and risk approval are ready.

Ignoring auditability

Every important AI-assisted workflow should leave a trail: input, output, data source, user, timestamp, and reviewer action.

Over-automating regulated decisions

KYC, AML, fraud enforcement, and credit decisions need careful governance. AI can support the process, but final accountability must stay with the bank.

Final Thoughts

Arabic LLMs for banking can help GCC financial institutions improve KYC, AML, fraud detection, customer support, risk review, and compliance operations. The opportunity is real, especially in Saudi Arabia, the UAE, and Qatar, where Arabic-first digital banking experiences matter.

But banking AI must be secure, explainable, localized, and supervised.

Planning Arabic LLMs for banking in Saudi Arabia, the UAE, or Qatar? Contact Mak It Solutions to design a secure, GCC-ready AI strategy for KYC, AML, fraud detection, customer support, and compliance workflows. Start with a consultation through the Mak It Solutions contact page and request a custom roadmap for your banking or fintech project.

FAQs

Q : Are Arabic LLMs suitable for Saudi banks regulated by SAMA?

A : Yes, Arabic LLMs can be suitable for Saudi banks when deployed with strong governance, customer-data protection, audit logs, and human approval workflows. The safest starting points are usually internal support, document summarization, KYC preparation, and fraud-alert triage.

Q : Can UAE banks use Arabic LLMs for AML and fraud monitoring?

A : Yes. UAE banks can use Arabic LLMs to support AML and fraud monitoring, especially for Arabic customer messages, suspicious activity summaries, and alert prioritization. The model should include explainability, escalation rules, and human review.

Q : How can Qatar banks use Arabic AI while meeting QCB expectations?

A : Qatar banks can use Arabic AI for customer support, KYC document review, risk summaries, fraud triage, and internal compliance knowledge search. They should document AI use cases, control access to customer data, test model accuracy, and maintain audit trails.

Q : Do Arabic LLMs work with GCC dialects and transliterated names?

A : Strong Arabic LLMs can handle many GCC dialect patterns and transliterated names, but banks should test this carefully before deployment. Names, abbreviations, family structures, and mixed Arabic-English messages can create false matches or missed risk signals.

Q : Should GCC banks choose a private Arabic LLM or a vendor AI platform?

A : It depends on risk, data sensitivity, budget, and internal AI maturity. A private Arabic LLM may suit banks with strict data-residency and customization needs. A vendor-managed AI platform may be faster for pilots if hosting, data usage, audit logs, security, and regulatory support are clearly defined.