GCC Proof of Payment Verification: Stop Fraud

GCC Proof of Payment Verification: Stop Fraud

GCC Proof of Payment Verification: Stop Fraud

Fake “paid” screenshots can look convincing. Proof of payment verification gives GCC support teams a safer way to check customer claims before approving refunds, wallet credits, subscription access, delivery release, or dispute decisions.

For teams in Saudi Arabia, the UAE, and Qatar, the safest approach is simple: never trust the image alone. Match transaction IDs, payment records, identity signals, timestamps, and audit logs before taking action.

What Is Proof of Payment Verification?

Proof of payment verification is the process of checking whether customer-submitted payment evidence matches reliable transaction records.

It helps support teams confirm three things.

Was the payment actually made?

Does it match the correct customer, order, amount, and date?

Is the evidence safe enough to support a refund, delivery, credit, or case closure?

This is also known as transaction proof validation, customer claim authentication, or digital evidence verification.

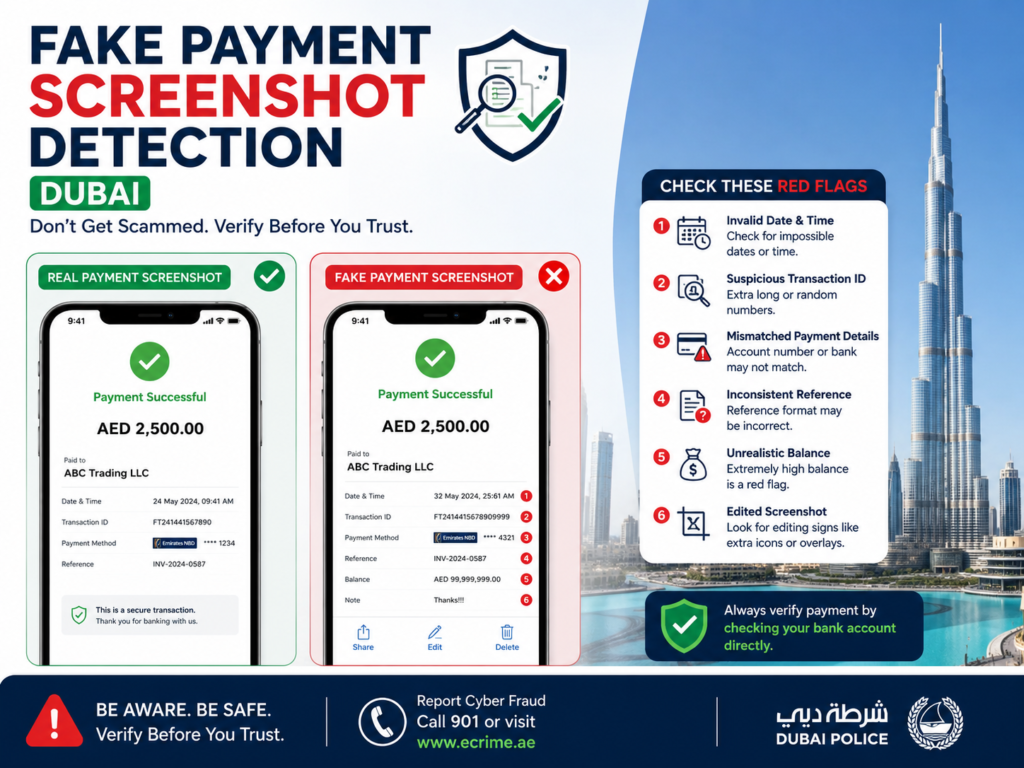

Why Screenshots Are Not Enough

A screenshot can start a support case, but it should not close one.

Payment screenshots are easy to crop, edit, compress, reuse, or forward through WhatsApp, email, live chat, and helpdesk tickets. A receipt may look polished and still be missing the real gateway status, bank confirmation, wallet reference, or settlement record.

The strongest proof is the data your system can verify, not the image a customer uploads.

What Counts as Valid Payment Proof?

In GCC support workflows, valid proof may include.

Transaction ID or payment gateway reference

Bank transfer number or wallet receipt

Order ID, invoice ID, or subscription ID

Sender name, IBAN details, or masked account details

Payment amount and timestamp

Customer account or identity signals

Backend gateway, PSP, bank, wallet, or ERP records

A screenshot can support the case, but the decision should come from verified records.

Why GCC Support Teams Face Higher Fake Proof Risk

WhatsApp-first support creates messy evidence

Many customers in Riyadh, Dubai, Abu Dhabi, Doha, and Jeddah expect fast mobile support. That usually means agents receive screenshots through chat instead of structured forms.

This is convenient for customers, but risky for businesses. Evidence gets scattered across channels, screenshots lose context, and agents may feel pressured to approve quickly.

Refund abuse can quietly damage margins

Fake proof does not always create one large loss. Often, it causes repeated small losses through.

Wrong refunds

Fake wallet top-ups

COD-to-paid conversion abuse

Unpaid delivery release

Marketplace seller disputes

Subscription access without settlement

For e-commerce, SaaS, fintech, delivery, and marketplace teams, these cases add up fast.

Arabic and bilingual flows matter

Arabic-speaking customers need clear instructions, Arabic-English labels, and simple examples of what to submit. In some Saudi workflows, date formats may also need extra clarity when Hijri and Gregorian dates appear in customer evidence.

A bilingual proof submission flow reduces confusion for customers and gives agents cleaner data to review.

How to Detect Fake Payment Screenshots

Check the basic details first

Start with simple checks.

Does the amount match the invoice?

Is the timestamp realistic?

Does the sender name match the customer account?

Is the transaction ID complete?

Does the order ID match the support case?

Has the same screenshot appeared before?

Many edited screenshots fail at this stage.

Compare the screenshot with trusted records

The next step is backend matching. Compare the submitted proof with your payment gateway dashboard, bank transfer log, wallet record, ERP, or order management system.

For Saudi teams, future-ready workflows may also consider SAMA’s Open Banking Framework, which includes business rules and technical standards for open banking use cases.

Use tamper signals carefully

Metadata, font mismatches, alignment issues, blurry transaction IDs, and compression artifacts can help agents spot suspicious proof.

But image analysis should only be a warning layer. It should not replace transaction matching.

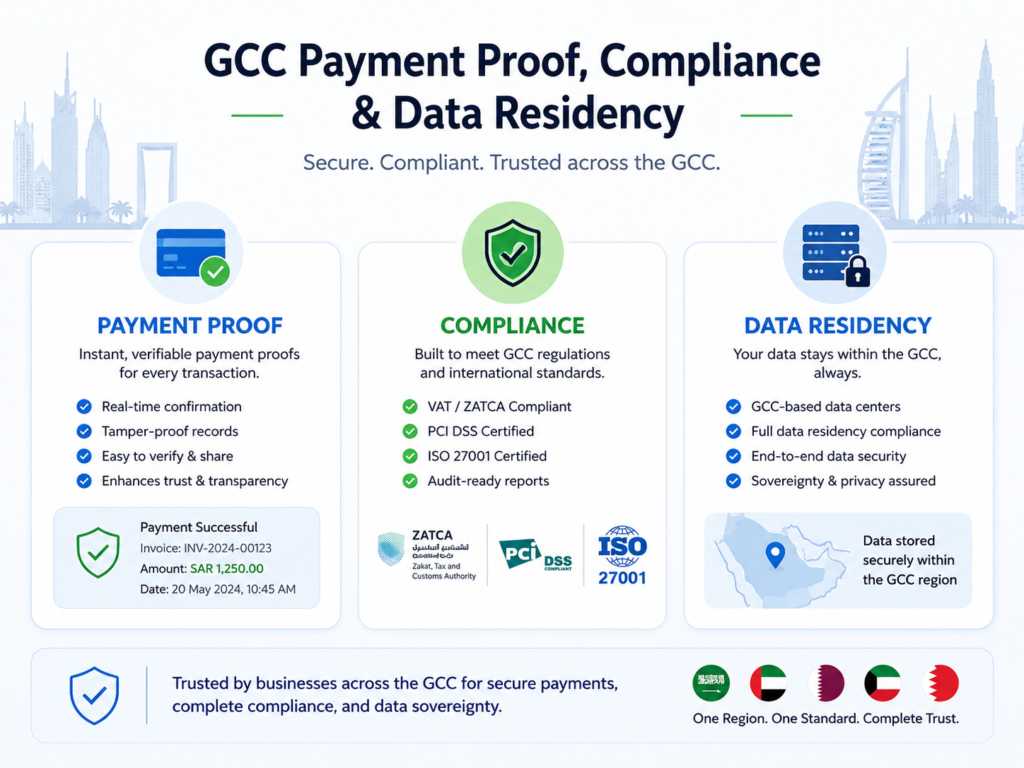

GCC Compliance and Data Protection Considerations

Payment proof often includes personal data: names, phone numbers, bank details, account references, transaction IDs, locations, and support notes.

That means proof of payment verification is not only a fraud-prevention workflow. It is also a data-handling workflow.

Saudi Arabia.

Saudi teams should collect only what they need, restrict access, and delete or retain evidence according to a clear policy. SDAIA notes that controllers have obligations around personal data protection, including destroying personal data after the purpose of collection has been fulfilled.

UAE.

In the UAE, higher-risk workflows may benefit from stronger identity assurance. TDRA describes UAE PASS as a secure national digital identity for citizens, residents, and visitors, with access across government and private-sector services.

For regulated financial workflows, the CBUAE Open Finance Regulation establishes requirements for licensing, supervision, and operation of the UAE Open Finance Framework.

Qatar.

Qatar companies should limit evidence collection, protect support logs, and define retention periods. Qatar’s privacy law includes provisions for protecting individuals’ privacy and personal data.

For regulated financial environments, QCB’s Data Handling and Protection Regulation treats technical information such as user credentials, network logs, system logs, application logs, and security logs as sensitive control areas.

This article is not legal or financial advice. Regulated businesses should confirm requirements with their compliance, legal, and security teams.

Proof of Payment Verification Workflow for GCC Teams

A practical workflow does not need to be complicated. It needs to be consistent.

| Stage | What the team should do |

|---|---|

| Customer submission | Ask for order ID, amount, payment method, transaction ID, and screenshot if needed |

| Consent and notice | Tell the customer why the proof is needed and how it will be used |

| Backend matching | Compare proof with gateway, bank, wallet, ERP, or order records |

| Identity check | Match the customer account, sender details, phone number, or verified identity signal |

| Risk review | Escalate suspicious, high-value, reused, or mismatched proof |

| Decision log | Record the evidence checked, agent action, approval, and outcome |

This protects honest customers too. Clear rules reduce back-and-forth and help agents make faster, fairer decisions.

Saudi Workflow for Made, Bank Transfers, and Support Tickets

For a Riyadh fintech, SaaS, or delivery team, a safe process may look like this.

Capture customer consent

Request transaction ID and order ID

Match Made, gateway, wallet, or bank transfer records

Compare customer identity signals

Approve, reject, or escalate the case

Keep an audit trail for disputes and internal reviews

The key rule is simple: no high-risk action should be approved from a screenshot alone.

UAE Workflow for Dubai E-Commerce and Refunds

A Dubai e-commerce brand should connect proof checks with order status, payment gateway records, refund policy, and customer identity.

For suspicious or high-value cases, agents should escalate before refund approval. Where identity assurance matters, UAE PASS-based journeys may support stronger customer claim authentication.

Teams building secure refund portals can connect this workflow with secure web development services and custom support systems.

Qatar Workflow for Doha Fintech and Customer Complaints

A Doha fintech, marketplace, or SME should match customer complaints with payment logs, transaction references, account history, and support timelines.

For cloud and data residency planning, businesses can assess regional options. AWS lists Middle East regions in Bahrain and the UAE, Microsoft lists Qatar Central in Doha along with UAE regions, and Google Cloud has a Doha region.

Choosing Proof of Payment Verification Software

Good proof verification software should reduce agent guesswork. Look for tools that support.

Arabic-English forms

Ticketing and CRM integration

Payment gateway matching

Duplicate claim detection

Refund approval workflows

Role-based permissions

Consent capture

Audit trails

SLA tracking

Case analytics and fraud dashboards

For reporting, dispute patterns, and agent performance visibility, business intelligence dashboards can help teams understand where fake proof risk is coming from.

For mobile-first businesses, in-app proof submission can also reduce messy WhatsApp evidence. That is where mobile app development services can support cleaner customer journeys.

Best Practices to Prevent Fake Proof Fraud

Create a no-screenshot-only policy

Make the rule clear: screenshots can support a case, but they cannot approve refunds, wallet credits, delivery release, subscription activation, or marketplace payouts on their own.

Train agents to spot red flags

Agents should know how to identify.

Mismatched amounts

Cropped sender names

Blurred transaction IDs

Reused receipts

Wrong timestamps

Urgent pressure tactics

Screenshots that do not match backend records

Move proof submission into structured forms

Instead of asking customers to “send proof,” use a secure form that requests the exact fields your team needs.

For e-commerce teams, this can connect with e-commerce development support so proof checks become part of order, refund, and delivery workflows.

Restrict access to sensitive evidence

Not every agent needs full access to customer payment proof. Use role permissions, masking, redaction, encryption, and access logs.

This reduces internal risk and supports better privacy governance.

Track every decision

Every case should show.

What evidence was received

Which records were checked

Who reviewed the case

Whether a supervisor approved it

What final action was taken

That audit trail becomes useful when customers dispute decisions or regulators ask how payment evidence is handled.

Final Takeaway

Proof of payment verification is not about assuming every customer is dishonest. It is about giving GCC businesses a fair, consistent, and privacy-aware way to handle payment claims.

Start with a no-screenshot-only policy, structured evidence forms, transaction ID matching, escalation rules, and audit logs. Then add API checks, identity signals, dashboards, and GCC data residency planning as your risk grows.

Mak It Solutions can help GCC teams design secure proof verification workflows for SaaS, fintech, e-commerce, logistics, and marketplace platforms. Explore Mak It Solutions services or contact the team to build a practical, GCC-ready verification strategy.

FAQs

Q : Can Saudi businesses accept screenshots as payment proof?

A : Saudi businesses can accept screenshots as supporting evidence, but they should not rely on screenshots alone for refunds, wallet credits, delivery release, or account activation. A safer approach is to verify the transaction ID, amount, timestamp, customer identity, and payment status against trusted records.

Q : What should UAE support teams check before approving a refund?

A : UAE support teams should check the order ID, payment gateway status, refund eligibility, customer identity, transaction reference, amount, and backend payment record. Suspicious or high-value cases should be escalated before approval.

Q : How can Qatar companies verify customer complaint evidence?

A : Qatar companies can verify complaint evidence by matching the customer’s claim with payment logs, transaction references, order history, account signals, and support-case timelines. Regulated businesses should also apply strong data handling, access control, and audit practices.

Q : Is proof of payment verification useful for GCC e-commerce teams?

A : Yes. Proof of payment verification helps GCC e-commerce teams reduce refund abuse, fake transfer claims, COD confusion, delivery release fraud, and marketplace disputes. It also improves customer experience because honest customers get clearer instructions and faster decisions.

Q : What is the safest way to handle customer screenshots?

A : Treat screenshots as personal data. Collect only what is needed, restrict access by role, redact unnecessary details, define retention periods, and log every support decision in a secure system.